Indicators for Q1 2014 show the economy began the year strongly, but the challenge remains to ensure the growth is sustainable. Michael Dall presents highlights of Barbour ABI’s latest monthly Economic & Construction Market Review, with a special focus on the infrastructure sector

Economic context

Figures from the Office for National Statistics (ONS) show UK GDP growth in Q1 2014 was 0.8%, making it the first time there has been five quarters of consecutive economic growth since 2007.

Although this growth was slightly lower than most forecasters predicted, it still equates to a strong start to the year for the economy. These figures mean that the UK has almost returned to pre-recession levels of economic activity. GDP is currently 0.6% below that recorded in Q1 2008, prior to the start of the economic decline.

The construction sector grew by 0.6% between Q4 2013 and Q1 2014, but it still remains 12% below the levels recorded in Q1 2008, prior to the start of the downturn

The latest unemployment figures also show a significant drop in the number of people out of work. Unemployment was at 2.21 million in January to March 2014, down by 309,000 from a year earlier. This means the unemployment rate is now 6.8%, the lowest since early 2009.

The latest forecasts from the Bank of England predict that GDP growth will be 0.8% in Q2 2014. The Bank is also confident that there is significant slack in the economy to allow it to grow without rapid inflation. It maintains the view that business investment will increase this year though there is little evidence of this in the official statistics so far.

If business investment does grow, the longer-term outlook for UK economic performance will be substantially improved.

Other news this month that supports the improving economic environment includes:

- The CBI Industrial Trends Survey showed the biggest upward shift in confidence levels since April 1973

- Car production rose 12% in March, providing a boost to exports

- A British Retail Consortium/KPMG survey showed retail sales increased by 4.2% in April

With the latest forecasts from the Bank and the continuing positive macroeconomic news, the economy seems well placed for a strong year. If the challenges of underemployment and low business investment are addressed, as the Bank suggests they will be, the long-term outlook will be more encouraging.

However, there is sparse evidence that this is happening at the moment, so it will be closely monitored this year to determine the sustainability of the economic recovery.

Barbour ABI believes that the near-term outlook for the economy has improved, but the challenges of addressing the output gap, the trade deficit and encouraging greater business investment will be vital to ensure sustainable economic growth in 2014 and beyond.

The construction sector’s performance

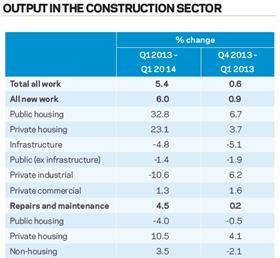

Latest figures from the ONS show that the construction sector grew by 0.6% between Q4 2013 and Q1 2014. This consisted of a strong January but weaker February and March.

Comparing Q1 output levels with the same period in 2013 showed an increase of 5.4%. However, output in the sector still remains 12% below the levels recorded in Q1 2008.

It is clear that the housing sector is driving growth in the industry. New private housing increased by 3.7% from the previous quarter and 23.1% from the corresponding quarter in 2013. At the same time, new public housing grew by 6.7% between Q3 2013 and Q4 2013 and 32.8% from Q4 2012. Output in the private commercial sector was slower in the first quarter of this year, increasing by 1.3% from Q1 2013. Infrastructure declined by 4.8% in the same period.

This highlights that growth patterns are focused on housing, and broader improvements are needed to ensure a robust recovery.

The CPA/Barbour ABI Index

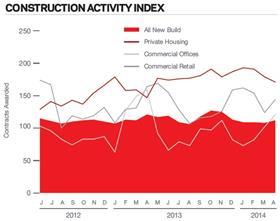

The CPA/Barbour ABI Index, which measures the amount of contracts awarded using January 2010 as its base month, recorded a reading of 112 for April. This is higher than recent months and continues to support the view that activity in the industry remains strong.

Although lower than recent months, the readings for private housing remained high. The figures for commercial offices continued their recent rise with a reading of 121 in April and commercial retail also rebounded to 144 after a dip in March.

According to Barbour ABI data on all contract activity, April recorded a fall in construction levels, with the value of new contracts awarded reaching £5bn based on a three-month rolling average. This is a decrease of 1.8% from March, but a 0.6% rise on the value recorded in April 2013, an indication of a boost in construction activity in the past year. The number of construction projects in April was down 6.6% on March, but 6.7% higher than April 2013.

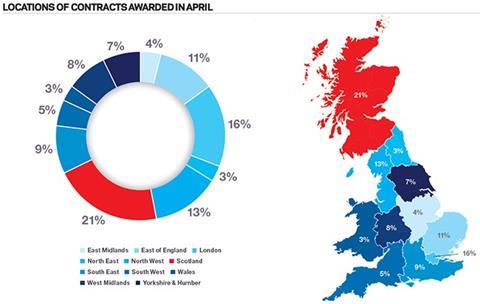

The majority of the contracts awarded in April by value were in Scotland, which accounted for 21% of the UK total. The main reason for this was the contract awarded for the Neart na Gaoithe 450MW offshore windfarm to be located off the Fife coast with a total contract value of £675m.

London was the next most prominent region, accounting for 16% of the contracts awarded in April, with major projects including a £200m residential development at Leamouth Peninsula in Poplar and a £95m commercial development Creechurch Place in the City of London.

Construction performance by sector

Spotlight on the infrastructure sector

The value of infrastructure contracts increased after recent monthly falls but there is still concern about longer-term growth. The value of contracts awarded in April rose to a total of £1.5bn based on a three-month rolling average. This is 57.7% higher than the previous month and 4.9% higher than April 2013.

In the three months to April, the total value of contract awards was £3.6bn based on a three-month rolling average. This is 38.7% lower than the previous three months and 24.9% lower than the same period in 2013.

This indicates a better month for infrastructure, but the longer-term decline in the value of activity is slightly concerning given the size of the sector.

Projects by region

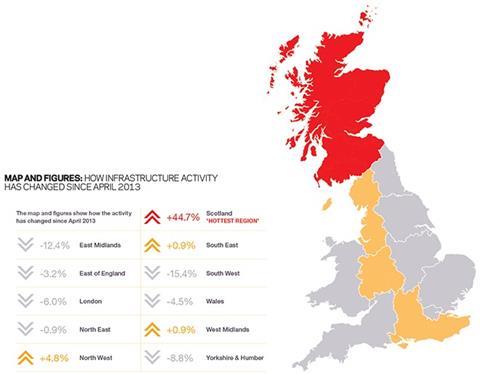

The main location of infrastructure projects in April was Scotland with 54.1% of the total value, an increase of 44.7% from April 2013. This is primarily due to the Neart Na Gaoithe offshore wind farm in Fife with an estimated value of £675m.

Yorkshire & the Humber was the other major location of infrastructure projects in April, accounting for 12.2% of projects awarded, an 8.8% decrease from the corresponding month last year.

Downloads

ECMR May 2014

PDF, Size 0 kb

1 Readers' comment