Oman’s strategic Vision 2020 couples social reform with economic diversification. With five years left to deliver the vision’s ambitious objectives, EC Harris explores Oman’s competitive construction market

01 / Introduction

Oman is the oldest independent state in the Arab world. It is an oil-rich country and 51% of GDP stems from this natural resource (2014). Oman has smaller oil reserves than other Middle Eastern countries, and recognises that they are finite, so it has begun the process of diversifying its economy to reduce reliance on oil. The Omani government aims to reduce reliance on oil to 9% of GDP by 2020.

Diversification seeks to capitalise on Oman’s strong traditions, rather than to efface them. For example, large infrastructure investments are in part aimed to improve access to the country by tourists, many of whom come to visit historical sites. The aim is to increase the numbers of visitors from 2 million to 12 million per year by 2020. Developments in Muscat, the capital, provide examples of the country’s twin initiatives: to modernise, as well as to protect Omani culture.

Oman’s geography is dominated by desert, which covers around 82% of its landmass, placing pressure on its urban centres. Three-quarters of Omanis reside in cities along

Oman’s coast, the highest density being in Muscat at 296 people per square km (2013). Urbanisation is intensified by Oman’s predominantly youthful population, 50.8%

of whom are aged 24 and under.

Coming to the main urban cities looking for education, employment and social opportunities, this demographic is consequently raising demand for educational facilities, as well as transport, leisure and technology. The country’s annual population growth of 4% is expected to continue to 2020 when the overall population will be 4.5 million, increasing the demand for a whole range of services.

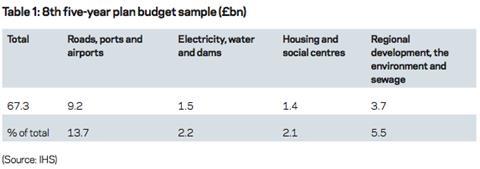

Vision 2020, is the strategy document that details Oman’s key objectives for economic stability, and places the emphasis on infrastructure investment alongside boosting the skills of the Omani workforce. It is a 25-year initiative, announced in 1995, and is now in its 8th five-year plan (2011-15). This £67.3bn phase aims to keep the rate of inflation low, and achieve an annual GDP growth of at least 3%. Currently the vision appears to be on track, with GDP growing 5.86% in 2014.

Oman’s location on the south-eastern tip of the Arabian Peninsula, with a 2,092km coastline, helps it act as a gateway to the Gulf, the Arabian Sea and the Gulf of Oman. Oman’s strategically important position makes it ideally placed on East to West trade routes.

The government is seeking to build on its free trade agreement with the United States (signed 2006) to open further trading.

02 / Economic and political outlook

Sultan Qaboos has ruled Oman by decree since 1970. He is yet to announce a successor. There has been some societal unrest in the country, though not on the scale seen elsewhere in the Middle East during the Arab Spring. There were protests against high levels of unemployment, lack of government accountability and slow reforms in 2011, with the Sultan responding by prioritising spending on social infrastructure, wage increases, and defence spending.

The largest spending during 2011 - 2015 will be on infrastructure (Table 1 shows an extract of allocated investment. Other investments include oil and energy production, health, education, and tourism). Oman is responding to its population growth, and the need for its people to have access to affordable housing, by ringfencing around £322.7m of the £1.4bn budget for housing and social centres for affordable housing.

This should yield around 12,000 additional affordable housing units, but will fall short of total affordable housing demand. In 2011 a shortage of around 15,000 housing units was identified, which will likely increase due to a rising population.

Oman’s investment in infrastructure denotes its drive to globalise its economy. Ease of movement into, and around, the region, reveal its priority to develop non-oil sectors like agriculture, fisheries, tourism, mining petrochemicals and industry.

Capital tends to be from the state-directed sources such as the Sovereign Wealth Fund, or the £309m given to Oman by the UAE (part of a £1.5bn pledge). Aligned with Oman’s Vision 2020, international engineering consultancies, like Arcadis and Aecom, are building relationships and portfolios across infrastructure sectors, including siting offices in the capital, Muscat.

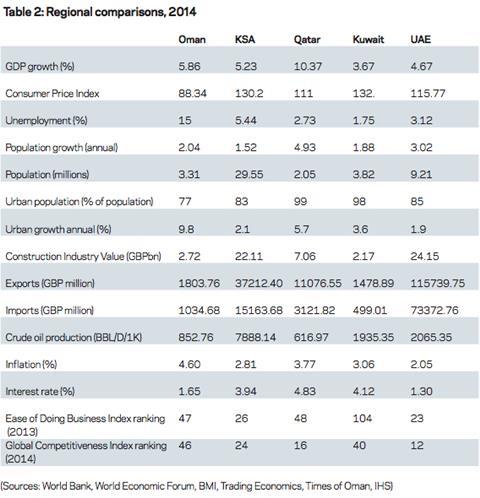

The country has introduced a number of changes to tax regulations and their overall legal framework in order to attract foreign investment. For instance, the corporate tax rate in Oman is 12%, in comparison with Saudi Arabia, which levies a 20% rate for non-Saudi companies. This friendliness to foreign investment has had a beneficial effect. However, as Table 2 indicates, Saudi Arabia substantially outstrips Oman in the Ease of Doing Business Index, influenced by lower levels of overall state bureaucracy that enable businesses to be set up more easily.

Oman has an overall positive economic outlook that results from a growth in domestic spending, which has been encouraged by a rise in the minimum wage for private-sector employees, and a lower rate of consumer price inflation than other GCC countries. However, the domestic market is somewhat limited, as unemployment remains higher in Oman than other GCC nations.

03 / Construction market

Forecasts show a steady increase in spending on the construction industry up to, and beyond, 2020. In 2014, £7.2bn is estimated to be spent on construction in total, rising to £7.8bn in 2015. Although the contribution that construction makes to GDP has come down to 4.9% in 2014 from 9% in 2010, Table 3 demonstrates that the sector is growing annually. The construction industry in Oman operates in an environment where:

- Foreign investors are not permitted to own land

- There is a 33% limit on the proportion of expat workforce

- Private-sector firms are required to meet quotas for hiring native Omani workers. If companies fail to employ enough nationals they can be prevented from operating in the country

- “Omanisation” of labour has resulted in a resources challenge in construction, as traditionally over a third of Oman’s migrant population work in the sector

- Health and Safety is a developing area, which requires further attention.

04 / Infrastructure

In 2014, the value of the construction industry grew by 6.41% and transportation infrastructure was the major driver of this growth, showing gains of 13.4%. Infrastructure construction is expected to increase by 6.2% in 2014, as the government pursues large-scale developments across transport, energy and desalination.

Oman offers opportunities in this sector, and Arcadis has found that Omani clients have robust procurement processes, with multiple layers of checking and verification, resulting in a prolonged period between flotation and award. This is believed to be partly due to the government’s drive to eliminate corruption from the procurement of services from contractors, consultants and other service providers.

Rail

There are no mainline railways in Oman but the building of a national rail network is one of the largest infrastructure projects in the country’s development pipeline. With an estimated cost of £12.4bn by the time it is operational in 2018, the 2,135km project will be implemented in nine phases, covering the length of the Sultanate. It will connect with the wider GCC network. The project is funded in part through GCC and state sponsorship. The Oman Rail Company leads the development within the country and recently called for tenders for phase one, with the expectation that construction will begin early 2015.

Roads

In the absence of a rail network, Oman is reliant on its road system. Sultan Qaboos has overseen huge expansion to Oman’s road network; there were only 10km of paved roads before 1970. Oman’s road infrastructure is now the fastest growing part of Oman’s transport infrastructure sector. The Ministry of Transport and Communication (MOTC) has a 25-year road network plan (2006-30), and 2013 alone saw companies submitting bids for more than £370m worth of roads projects. Further expansion continues - for instance, the Al Batinah Expressway is now in its second phase, and will cost approximately £1.6bn. The 265km-long, eight-lane road will link the capital, Muscat, to the new Sohar Port and industrial area, and extend up to the UAE border.

Ports

Strategically important for Oman’s economic diversification, industrial and commercial development in port cities has been a major factor in Oman’s drive to diversify. There has been large-scale expansion at Duqm Port, including the construction of a new port and dry-dock complex (due to be completed 2014), and the development of its surrounding facilities. This has cost around £1.1bn. There is also significant port construction elsewhere in Oman, such as the £80m expansion project at the Port of Sohar.

Airports

Investment in airports aims to have a beneficial impact on trade and tourism, as well as facilitating movement around the Sultanate. Infrastructure projects such as the development of Muscat International Airport support these objectives. Three further phases of development are planned at Muscat International, eventually boosting its already large capacity of 12 million passengers per year to 48 million by 2050. In addition to the vast expansion of Muscat International Airport in the North-east, an airport opened in Duqm in the south-east in July 2014, although construction continues on its third phase.

Water

Investment in water desalination, waste and power is essential in Oman, especially if the country is to meet the needs of its growing population. Water, power and waste disposal are all part-privatised in Oman, but the proposed large-scale Qurayat desalination project will have a 20-year water purchase agreement with the state-run Oman Power and Water Procurement Company. Bids for this project were opened in September 2014. The winner will build, own and operate a facility with the capacity to produce 200,000m3 per day of potable water, which is expected to start operating by the second quarter of 2017.

Commercial sector

Oman’s emphasis on growing tourism has resulted in high levels of commercial construction. Muscat forms a primary example, as its mass redevelopment under the Majestic Muscat banner will lead to 24 mega-projects. These projects include hotels, conference centres and the regeneration of Muscat’s waterfront. For example, the Seeb Waterfront, the Al Mawaleh Souk and the Sultan Qaboos Boulevard. Alongside tourism is the development of office space, which has experienced its highest level of growth to date. This reflects a growing demand from both domestic and international companies, including HSBC, which has 88 branches in the country.

Social

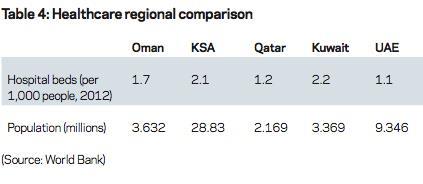

Spurred by protests during the Arab Spring in 2011, recent years have witnessed a boost in social infrastructure investment in Oman - contributing to the existing programme that has occurred since 1970. The country now has over 1,000 schools and over 20 colleges and universities, both private- and state -funded, compared to two in 1970. Omani citizens receive free health care, and there are over 500 hospitals and clinics in the country, also up from two in 1970. Considering Oman is seen as a “less mature” economy than some of its regional neighbours, its healthcare system is well developed (see Table 4).

Residential

Demand for affordable housing is likely to increase in tandem with Oman’s population, which is dominated by a high-proportion of young people. Even though one out of every five Omani families in Muscat and North Batinah own their houses, there is a shortage of properties for low-income persons in Muscat’s rental market. While the eighth phase of “Vision 2020” plans to build 12,000 affordable homes, there are also prime residential projects in the pipeline - again focused around urban areas like Muscat. For instance, Saraya Bandar Jissah’s £371m Integrated Tourism Complex (part of Majestic Muscat) will offer 398 high-end housing units, spread across five residential zones.

Water

Investment in enhanced oil-recovery technology is helping Oman to exploit its depleting oil reserves, yet it is also developing its capacity to produce other energy sources.

Oman’s ability to grow this sector has been enabled by oil revenues, and therefore falling oil prices in the global market could have a negative impact on Oman’s short-term economy. Oman’s investment in new technologies, like enhanced oil-recovery, seeks to maintain their short-term revenue stream.

The country is also advancing its renewable energy sources, and aims to use renewables to meet 10% of its energy demand by 2020. The European companies Terra Nex and Middle East Best Select have been employed to build a solar power plant valued at over £1.2bn.

05 / Outlook

Vision 2020 is driving Oman’s response to the need to diversify, facilitating substantial growth, which is creating many opportunities in the construction sector. Increased variety in the economy is likely to lead to further construction contracts, and investment in auxiliary infrastructure. Predictions for the medium-term outlook assert that the fastest-growing segment will be non-residential structures construction.

Oman will face challenges over the coming years, as oil still occupies a major percentage of the country’s GDP, and its ambitious plans to dramatically reduce its reliance on oil will need to be effectively instigated, tendered and programme managed to enable realisation by 2020. Meanwhile, as the Omani government negotiates between friendliness to foreign investors, and meeting the demands of its populace, it is likely that Oman’s vision to globalise its economy will need to overcome further hurdles. Hurdles will be around supply chain assurance, access to raw materials, attracting foreign investors and international construction companies to help build a diverse economy.

Yet while Oman’s depleting oil reserves and Sultan Qaboos’ delay in announcing a successor are creating some uncertainty, Oman is a fiercely competitive market and ranks fairly well in the World Economic Forum’s Global Competitiveness Indices.

At the time of writing, proposals need to be priced very keenly for a chance of being successful in the infrastructure consultancy services field. Dialogue with contractors has revealed the same with companies seeking to maintain staff, labour and equipment resource levels to sustain business until the workload increases to meet the aspirations outlined in Oman’s Vision 2020.

Acknowledgements

Thanks are due to John Maziliauskas, country manager, Arcadis Oman, whose insight was valuable in the completion of this piece. Data sources used for this article included: World Bank, World Economic Forum, IHS Construction Reports, Energy Information Administration & Business Monitor International, as well as trade and press articles.

No comments yet