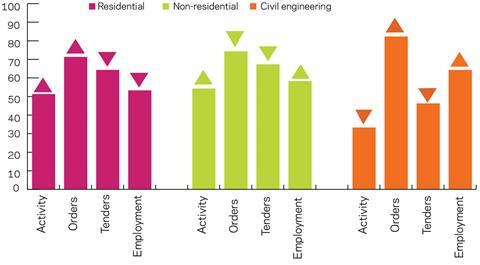

Activity indices rose in August for all sectors except civil engineering, which hit its lowest level for six months – this sector did, however, see the strongest growth in new orders although it was the only area in which tender enquiries actually fell

01 / State of play

Both the total activity and R&M activity indices remained above the no-growth bound in August. The former turned positive after gaining three points over July’s figure to reach 51. The R&M index gained two points and stood at 53.

The residential activity index ticked up by a point to 51, while non-residential recovered by six points to 54. Civil engineering remained in the negative, however, after falling nine points to 33, marking its lowest level since February 2018.

Orders and tender enquiries remained strong in August, as both indices gained momentum. The orders index grew by three points to 69 and the tender enquiries index gained four points to 65.

The biggest improvement by sector was seen in civil engineering, as its orders index added 22 points to its July figure to stand at 82. Residential orders also accelerated as the index gained four points to 71. The non-residential orders index also stayed high at 74 despite losing three points.

Falling indices

All three sector indices for tender enquiries fell in August (uplift in specialised construction orders, for which we do not provide a breakdown, supported the overall rise). The largest drop was in civil engineering, which fell nine points into negative territory at 46. The other two sectors remained positive. The residential enquiries index was 64 and the non-residential stood at 67, after losing three and one points respectively.

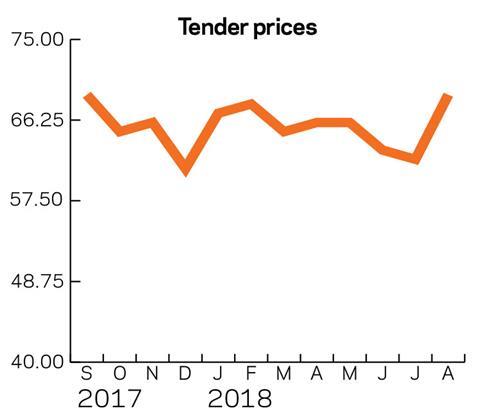

Tender prices rose in August as the index gained seven points to 69, its highest level since June 2017.

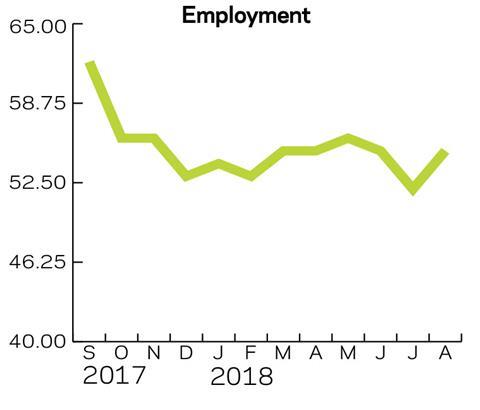

The employment prospects index gained three points in August to return to the June level of 55, marking its 13th consecutive month of growth.

Forty-eight percent of respondents faced no constraints in August, up on July’s 35%. Those reporting insufficient demand decreased by five percentage points to 20%, while 11% experienced financial difficulties, down from 16% in July. The share facing labour shortages remained almost unchanged – 12% compared with 13% in July.

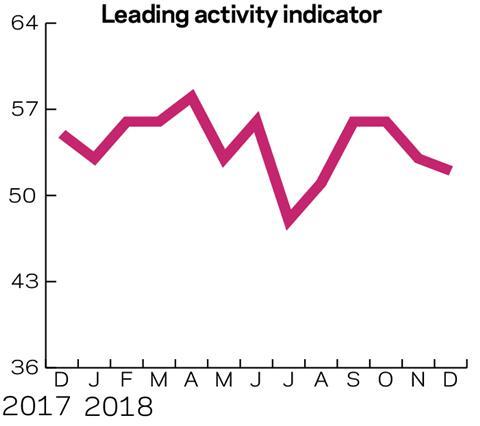

02 / Leading construction activity indicators

The total activity index returned to positive territory, just above the no-growth threshold at 51, after gaining three points over July’s figure. The acceleration is expected to continue over the next two months, with the index returning to its June level before losing some momentum. The R&M index increased its margin above the no-growth bound in August as it gained two points to stand at 53.

03 / Materials costs

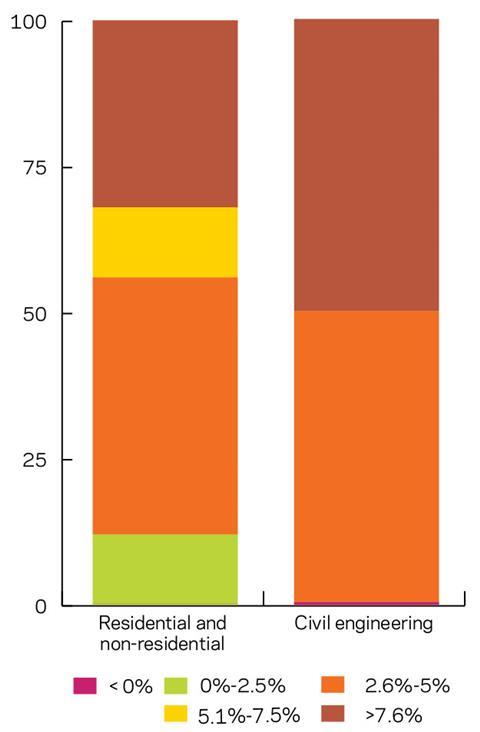

According to respondents in the residential and non-residential sectors, materials costs have been on the rise and accelerating in the last three months. None of the respondents have reported a decrease in costs, compared with 7.1% in May. The share of respondents incurring materials cost price rises of up to 5% has shrunk to 56% (down from 64.3% in May), on account of an increase in those reporting costs rising by more than 5% – up from 28.6% in May to 44% in August. In addition, almost one-third of respondents (32%) reported costs increasing by more than 7.5%, up from 25% in May.

Similar developments were observed in the civil engineering sector. All respondents have experienced materials costs growing by more than 2.5%, while in May 25% of the respondents reported a decrease. The acceleration is apparent as half of sector respondents in August reported changes exceeding 7.5% over the past three months, up from 25% in May.

04 / Regional perspectives

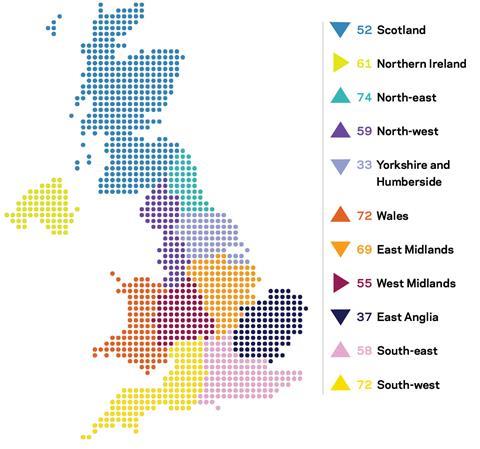

Experian’s regional composite indices incorporate current activity levels, the state of order books and the level of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

Yorkshire and Humberside was the worst performing region with an index of 33, after losing three points, followed by the East of England at 37, down by five points. The other two regions that lost some momentum were the East Midlands and Scotland. Despite seeing a downtick in both their indices by a point, they remained in positive territory at 69 and 52 points, respectively.

The fastest-growing region was the North-east, which gained six points to 74. Second place was shared by Wales and the South-west, as their indices gained two points each to 72. The North-west and South-east were the other two regions that accelerated slightly, as their indices increased by three and two points to reach 59 and 58. The indices for the West Midlands and Northern Ireland remained flat in August, keeping their July levels of 55 and 61, respectively.

The UK composite index recorded a decrease of two points to 51, barely staying in positive territory as a result of the regional developments. August nonetheless marks the sixth consecutive month of growth in the UK according to the composite index.

This an extract from the monthly Focus survey of construction activity undertaken by Experian Economics on behalf of the European commission as part of its suite of harmonised EU business surveys. The full survey results and further information on Experian Economics’ forecasts and services can be obtained by calling 0207-746 8217 or logging on to .

The survey is conducted monthly among 800 firms throughout the UK and the analysis is broken down by size of firm, sector of the industry and region. The results are weighted to reflect the size of respondents. As well as the results published in this extract, all of the monthly topics are available by sector, region and size of firm. In addition, quarterly questions seek information on materials costs, labour costs and work-in-hand.

1CFR’s Leading Construction Activity Indicator incorporates a range of factors to assess the construction industry’s prospects over the next quarter. The indicator is put together using information about past levels of activity, orders and tender enquiries

No comments yet