Construction activity remains consistent as the index picks up five points for the month, while the orders index sees a small incline and residential experiences a significant uptick

01 / State of play

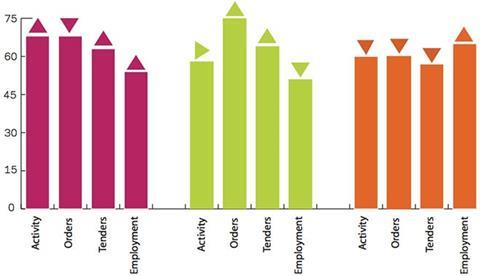

The construction activity index picked up by five points in July to reach 62. It points towards a sustained increase in construction activity sentiment. Performance was mixed at the sector level, with the residential one seeing a significant uptick on a monthly basis. Conversely, civil engineering saw a fall, while the non-residential one flattened out.

The orders index climbed three points to reach 68 in July; this was the 10th consecutive month of above average orders. Tender enquiries were also up, rising 12 points to 62, their highest value since the beginning of the year.

The proportion of respondents indicating that labour shortages were restricting productivity increased to 18% in July. Those experiencing no constraints on activity rose to 32%, while financial constraints became less of a factor, down to 10%.

Material/equipment shortages remain of little worry, as only 5% of respondents were concerned. Meanwhile, insufficient demand remained a significant factor, at 18%, up 13 percentage points since the corresponding period of 2013.

Bad weather has been of negligible concern, with <1% of respondents flagging it as an issue.

The employment prospects index was down slightly on a month-by-month basis, with a decrease of one point to 54. Despite a fall in prospects, its sustained strength indicates that businesses expect employment levels to rise over the coming three months.

Tender prices saw little change in July, falling by one point to reach 65. Prices remained above the 60-mark for the sixth consecutive month.

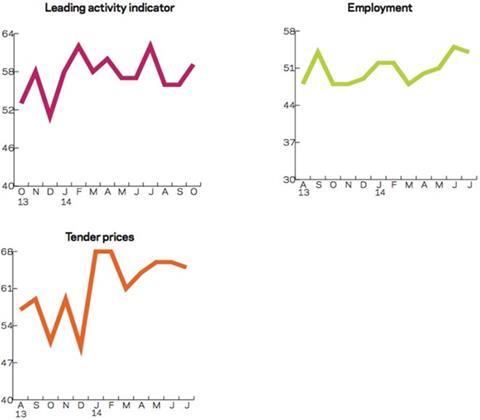

02 / Leading construction activity indicator

CFR’s Leading Construction Activity Indicator1 picked up to 62 in July, its highest figure since February, it was also the 19th successive month of above average activity, supporting the notion of a sustained upswing within the industry.

The indicator uses a base level of 50: an index above that level indicates an increase in activity, below that level a decrease.

03 / Labour costs

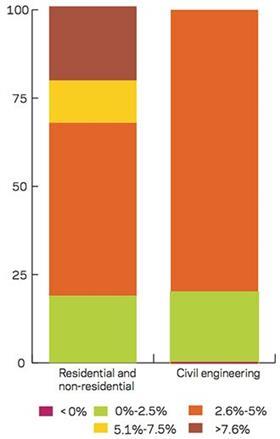

During July 2014, none of the residential respondents reported a reduction in labour costs. About 20% of respondents experienced labour cost inflation below 2.5%, down from April’s reported 33%. The percentage of respondents indicating that their labour costs had grown by between 2.6% and 5% rose to 49% in July, up from 37% in April. The percentage of respondents indicating that their wage bill had risen by between 5.1% and 7.5% remained at the same level as reported three months earlier (12), while the share of firms who experienced labour cost growth of more than 7.6% increased significantly to 17%.

04 / Regional perspectives

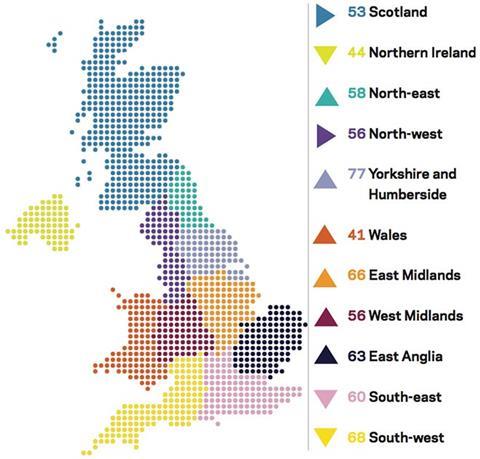

Experian’s regional composite indices incorporate current activity levels, the state of order books and the number of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

In July, six of the 11 regions and devolved nations saw their indices improve. Yorkshire & Humberside saw the largest increase with a 20-point upswing to 77. The East Midlands experienced a six-point uptick to 66. Despite Wales’ index climbing 11 points, it consistently remains rooted in negative territory. Moderate gains were also seen in East Anglia and the West Midlands, rising to 63 and 56 respectively.

Both the North-west and Scotland saw their indices remain stagnant in July, while the North-east climbed two points to reach 58. The South-west remained strong, despite falling one point to 68.

The South-east experienced the largest downturn, (-2 points), though the region stayed firmly in positive territory at 60. Northern Ireland posted a decline of one point; remaining in negative territory at 44.

As a whole, the UK index, which includes firms working in five or more regions, saw its index climb by two points to 62.

This an extract from the monthly Focus survey of construction activity undertaken by Experian Economics on behalf of the European commission as part of its suite of harmonised EU business surveys. The full survey results and further information on Experian Economics’ forecasts and services can be obtained by calling 0207-746 8217 or logging on to .

The survey is conducted monthly among 800 firms throughout the UK and the analysis is broken down by size of firm, sector of the industry and region. The results are weighted to reflect the size of respondents. As well as the results published in this extract, all of the monthly topics are available by sector, region and size of firm. In addition, quarterly questions seek information on materials costs, labour costs and work-in-hand.

1 CFR’s Leading Construction Activity Indicator incorporates a range of factors to assess the construction industry’s prospects over the next quarter. The indicator is put together using information about past levels of activity, orders and tender enquiries.

No comments yet