The annual building cost index continues to rise, with wages going up slightly. However, metal prices are generally falling. David Holmes of Davis Langdon, an Aecom company, reports

01 / KEY CHANGES

- Eurozone emerges from recession after 18 months of economic contraction with a 0.3% rise in the second quarter of 2013

- Metal prices continue to fall

- Industry input and output inflation bounce back slightly after falling in May and June

- Consumer price inflation fell in July 2013

- Construction materials prices remain subdued

- Steel price continues to fall

- New BATJIC wage agreement started in June.

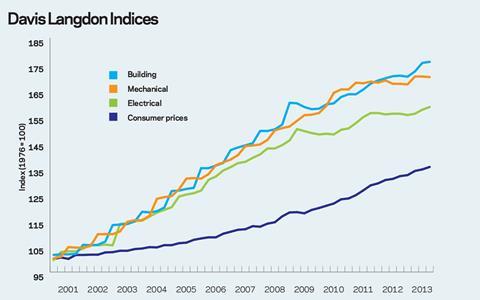

The following chart shows how Davis Langdon’s index series, reflecting cost movements in different sectors of the construction industry, have fared since 2000, with the movement of the Consumer Prices Index for comparison.

Percentage change year-on-year (Q2 2012 to Q2 2013)

| % | Direction | |

|---|---|---|

| ��ɫ����TV cost index | +3.1 | ▲ |

| Mechanical cost index | +1.6 | ▲ |

| Electrical cost index | +1.5 | ▲ |

| Consumer prices index | +2.8 | ▼ |

| (Q2 2013 figures are provisional) | ||

��ɫ����TV cost index

The 2% pay award to building operatives in January 2013 contributed to a rise of 1.9% in Q1 2013, leading to a jump in the annual figure to 3.1%.

Mechanical cost index

The index rose by 1.65% year on year. This increase is partly due to increased pension payments by employers for operatives together with some minor allowances increases.

Electrical cost index

There was a year-on-year increase of 1.5%, which is slightly lower than shown in May. Electricians received a 1.5% pay rise in January.

Consumer prices index

The fall to 2.4% in April has been reversed between May and June, rising to 2.9%, and is at 2.8% for July.

Guide to data

Davis Langdon’s cost indices track movements in the input costs of construction work in various sectors, incorporating national wage agreements and changes in materials prices as measured by government index series. They provide an underlying indication of price changes and differential movements in the various work sectors but do not reflect changes in market conditions affecting profit and overheads provisions, site wage rates, bonuses or materials price discounts/premiums. Market conditions are recorded in Davis Langdon’s quarterly Market Forecast (last published 19 July).

02 / COMMODITY PRICES

Price adjustment formulae indices, compiled by the ��ɫ����TV Cost Information Service (previously by the Department for Business, Innovation and Skills), are designed for the calculation of increased costs on fluctuating or variation of price contracts. They provide useful guidance on cost changes in various trades and industry sectors and on the differential movement of work sections in Spon’s Price Books.

Over the last 12 months between July 2012 and July 2013, the 60 building work categories recorded an average rise of 1.2%, up marginally from the 1.1% reported three months ago.

Of the 60 work categories published, 50 show a price increase over the last 12 months. The largest price increases over the last year have been in the following work categories:

| Oct 2011 - Oct 2012 | % change |

|---|---|

| Waterproofing: asphalt | +3.4 |

| Finishes: plaster | +2.8 |

| Boards, fittings and trims: manufactured | +2.7 |

| Softwood carcassing and structural members | +2.7 |

| Claddings and covering: GRP | +2.6 |

| Finishes: painting and decorating | +2.5 |

The largest fallers are:

| Oct 2011 - Oct 2012 | % change |

|---|---|

| Piling: steel | -0.8 |

| Pipes and accessories: spun and cast iron | -0.8 |

| Metals: miscellaneous | -0.9 |

| Insulation | -1.0 |

| Cladding and covering: copper | -1.1 |

| Finishes: bitumen, resin and rubber latex flooring | -1.8 |

| Concrete: reinforcement | -3.1 |

The biggest price falls are associated with steel materials with reinforcement prices dropping the most by far.

Materials: Metal prices continue to decline due to the slowdown in China

03 / EXECUTIVE SUMMARY

- Industry input costs rise ▲

- Output prices rise 2.1% in the year to July ▲

- Metals prices slide ▼

| Consumer prices | % change June 2012 - July 2013 | Direction |

|---|---|---|

| Consumer price index | +2.8 | ▼ |

The annual rate in July fell to 2.8% from 2.9% in June. The index has risen 0.7% since the end of 2012. The rate of retail prices index (RPI) inflation also fell, to 3.1%, from 3.3% in June.

Industry input costs

Since autumn 2011 the price of materials and fuels purchased by the UK manufacturing industry fell from an annual inflation of around 18% to deflation of around 2% in the middle of 2012.

| % change Jun 2012-Jun 2013 | ||

|---|---|---|

| Materials and fuels purchased by manufacturing industry | +4.2 | ▲ |

| Materials and fuels purchased by manufacturing industry excluding food, beverages, tobacco and petroleum industries | +2.1 | ▲ |

Between May and June the total input price index rose by 0.2% compared with a fall of 0.6% between April and May. The biggest decreases were in fuels and imported metals at -1.7% for each. Between June and July the input price index rose 1.1% with the biggest rises of 6.8% in crude oil and fuels at 2.1%. Key price movements over the last year to July have been:

| Electricity | +7.6 |

| Gas | +11.1 |

| Imported metals | -3.3 |

| Imported plastic products | +3.3 |

| Imported wood and wood products | +2.2 |

| Imported glass and glass products | +4.8 |

Industry output prices

Factory gate inflation now stands at 2% for the year, an increase of 0.1% on the lower inflation rates seen in April and May 2013.

| Output prices of manufactured products | + 2.0 ▲ |

| Output prices of manufactured products excluding food, beverages, tobacco and petroleum | +1.0 ▲ |

| Metals prices | % change Feb 2013 - July 2013 | Direction |

|---|---|---|

| Copper | -11.0 | ▼ |

| Aluminium | -11.3 | ▼ |

| Lead | -9.5 | ▼ |

Metals prices continue to fall back since February as concerns over the economic slowdown in China, the top buyer of base metals.

Exchange rates

| Jul 2013 average | Jul 2013 average | % change | |

|---|---|---|---|

| Euro to sterling | 1.269 | 1.160 | -8.6 |

| US dollar to sterling | 1.559 | 1.517 | -2.7 |

The British pound lost a fair bit of ground over the past year both against the euro and the US dollar, mainly due to diverging global central bank policy and uneven recovery dynamics in the US and European market.

Construction industry

Materials price increases for the construction industry over the last year (to June 2013) are detailed below:

| % change Jun 2012 - Jun 2013 | Direction | |

|---|---|---|

| Construction materials generally: | ||

| New housing | +0.8 | ▶ |

| Non-housing new work | +0.6 | ▶ |

| Repair and maintenance | +0.5 | ▶ |

There was some increase in materials prices at the start of the year, particularly for new housing and repair and maintenance, which show an increase over 1%but, year on year, prices are still relatively subdued.

| Mechanical services materials | % change Jul 2012 - Jul 2013 | Direction |

|---|---|---|

| Housing only | +0.5 | ▶ |

| Non-housing | 0.0 | ▶ |

| Electrical services materials | 0.0 | ▶ |

Mechanical and electrical materials prices have fallen a little over the year but are generally stable.

A few materials have shown above or below average price movement over the last year:

| Jun 2012 - Jun 2013 * | |

|---|---|

| Sand and gravel | +5.1 |

| Insulating materials | +3.8 |

| Plastic pipes (rigid) | +3.4 |

| Concrete reinforcing bars | -5.3 |

| Metal sections | -4.9 |

| Steel for reinforcement | -7.6 |

(*Jun 2013 figures provisional, Data sources: ONS and BIS)

Annual construction material price inflation rose to 0.5% in June following a fall of 0.1% in May.

Labour: A new wage agreement took effect in June, giving some workers a 2% pay increase

05 / EXECUTIVE SUMMARY

- Average weekly earnings in the construction industry in the second quarter of this year rose to £533, an increase of 2.1% over the previous quarter

- Average weekly earnings throughout the whole economy rose by 1.1% compared to April to June 2013 to £447 before taxes and deductions, up from £443 a year earlier

- In the first quarter of 2013, the number of people in construction jobs rose to 1.9 million, an increase of 0.6% from the end of 2012.

06 / WAGE AGREEMENTS

��ɫ����TV and Allied Trades Joint Industrial Council (BATJIC) agreed new wage rates, which came into effect on 17 June 2013. The 2013/14 agreement involves a 2% increase in pay. The rise is across the board except for the hourly rate for the adult general operative, which increases by 3% from £7.96 to £8.20 per hour. There are also improvements in the death benefit scheme, which increases to £25,000, and statutory sick pay rises to £119 per week.

The new BATJIC rates of wages are:

| Standard rates of pay for 39hrs per week | Per week | Per hour |

|---|---|---|

| S/NVQ3: Advanced | £426.66 | £10.94 |

| S/NVQ2: Intermediate | £366.60 | £9.40 |

| Adult general operative | £319.80 | £8.20 |

| For entrants aged 19 years and over: | ||

| Third 12 months with NVQ2 | £344.37 | £8.83 |

| Third 12 months without NVQ | £299.52 | £7.68 |

| Apprentices under 19 years of age: | ||

| 18 years of age with NVQ2 | £299.52 | £7.68 |

| 18 years of age without NVQ2 | £283.14 | £7.26 |

06 / WAGE AGREEMENTS

��ɫ����TV and Allied Trades Joint Industrial Council (BATJIC) agreed new wage rates, which came into effect on 17 June 2013. The 2013/14 agreement involves a 2% increase in pay. The rise is across the board except for the hourly rate for the adult general operative, which increases by 3% from £7.96 to £8.20 per hour. There are also improvements in the death benefit scheme, which increases to £25,000, and statutory sick pay rises to £119 per week.

WAGE AGREEMENT SUMMARY

The following table summarises the wage agreements currently in force for the principal wage fixing bodies within the construction industry

| Operatives | Agreement body | Current basic hourly rate | Effective since | Details in | Date of next review |

|---|---|---|---|---|---|

| Builders and civil engineering operatives | Construction Industry Joint Council | Craft rate: £10.67 / hour | 7 January 2013 | Cost Update 1 March 2013 | Not before 2 January 2014 |

| ��ɫ����TV and Allied Trades Joint Industrial Council (BATJIC) | S/NVQ3 advanced craft: £10.94 / hour | 17 June 2013 | Spon’s Architects’ and Builders’ Price Book 2014 | Agreement until 15 June 2014 | |

| Plumbers | The Joint Industry Board for Plumbing Mechanical Engineering Services in England and Wales | Advanced plumber: £13.50 / hour | 2 January 2012 | Spon’s Architects’ and Builders’ Price Book 2014 | Expected 7 January 2013 - discussions continue |

| Scottish and Northern Ireland Joint Industry Board for the Plumbing Industry | Advanced plumber: £12.89 / hour | 6 June 2011 | Spon’s Architects’ and Builders’ Price Book 2014 / Cost Update 27 May 2011 | Negotiations ongoing for 2013-14 | |

| H&V operatives | Joint Conciliation Committee of the Heating, Ventilating and Domestic Engineering Industry | Craftsman: £11.55 / hour | 1 April 2013 | See above | 7 April 2014 |

| Electricians | The Joint Industry Board for the Electrical Contracting Industry / Scottish Joint Industry Board for the Electrical Contracting Industry | Approved electrician: £14.57 / hour (own transport) | 7 January 2013 | Cost Update 1 March 2013 | 6 January 2014 |

No comments yet