The consumer price inflation rate dips into negative territory on a single-month basis for the first time in recorded history. Michael Hubbard of Aecom reports

01/ Key changes

- Construction materials cost inflation picked up in Q1 2015 across all indices.

- Consumer price inflation was just 0.1% annually when averaged over Q1, but dropped below zero in April for the first time in recorded history.

- Average weekly earnings for the construction sector outperformed the same measures for the economy as a whole.

- Industry input costs remained firmly negative with slight improvement in output price levels during Q1 2015.

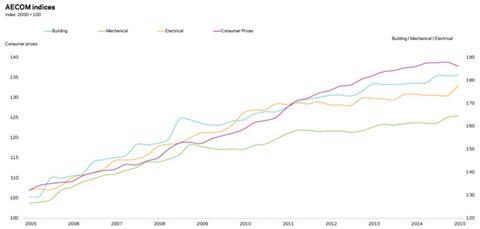

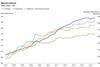

The following chart shows Aecom鈥檚 index series since 2005, reflecting cost movements in different sectors of the construction industry and consumer prices.

Percentage change year-on-year (Q1 2014 to Q1 2015) | ||

|---|---|---|

| % | Direction | |

| 好色先生TV cost index | +1.9 | 鈻� |

| Mechanical cost index | +1.8 | 鈻� |

| Electrical cost index | +2.1 | 鈻� |

| Consumer prices index | +0.1 | 鈻� |

| (Q1 2015 figures are provisional) | ||

好色先生TV cost index

好色先生TV costs increased in the year to Q1 2015 by 1.9%. Labour cost inflation led to most of the yearly increase.

Mechanical cost index

The rate of annual change at Q1 2015 remained constant at 1.8%. Labour cost inflation contributed more to the yearly increase, but with some contribution from materials too.

Electrical cost index

The electrical cost index rebounded in Q1 2015, increasing by 2.1% over the year. The index mirrors changes to metals commodities prices recorded over Q1 2015.

Consumer prices index

The consumer price inflation (CPI) rate was just 0.1% at Q1 2015. On a single-month basis, though, CPI dipped into negative territory for the first time in recorded history in April 2015.

Guide to data

Aecom鈥檚 cost indices track movements in the input costs of construction work in various sectors, incorporating

national wage agreements and changes in materials prices as measured by government index series.

They are intended to provide an underlying indication of price changes and differential movements in the various

work sectors but do not reflect changes in market conditions affecting profit and overheads provisions, site wage

rates, bonuses or materials鈥� price discounts/premiums. Market conditions and commentary are outlined in Aecom鈥檚

quarterly Market Forecast (last published April 2015).

02/ Price adjustment formulae for construction contracts

Price Adjustment Formulae indices, compiled by the 好色先生TV Cost Information Service are designed for the calculation of increased costs on fluctuating or variation of price contracts. They provide guidance on cost changes in various trades and industry sectors - i.e. those including labour, plant and materials - and on the movement of work sections in Spon鈥檚 price books.

The 60 building work categories saw an average decrease of 0.4% on a yearly basis. Higher rates of change were seen in the following categories:

Price adjustment formulae | |

|---|---|

| Apr 2014 - Apr 2015 | % change |

| Windows and doors: aluminium | 5.4 |

| Pipes and accessories: clay and concrete | 4.9 |

| Pipes and accessories: aluminium | 4.8 |

| Cladding and covering: aluminium | 4.5 |

| Brickwork and blockwork | 3.9 |

| Concrete: in-situ | 3.4 |

| Pavings: slab and block | 2.9 |

The largest price decreases include:

Price adjustment formulae | |

|---|---|

| Apr 2014 - Apr 2015 | % change |

| Metal: decking | -9.1 |

| Piling: steel | -6.7 |

| Cladding and covering: coated steel | -6.2 |

| Concrete: reinforcement | -5.7 |

| Waterproofing: asphalt | -4.2 |

| Raised access floors | -3.8 |

| Pipes and accessories: copper | -3.5 |

Materials

03/ Summary

- Consumer price inflation turned negative for the first time since 1960 鈻�

- Manufacturing input prices continue to fall 鈻�

- Industry output prices remain in negative territory 鈻�

- Metals prices fell again but began to rebound at the end of Q1 2015 鈻� 鈻�

- Construction materials price inflation mainly related to housing sector activity 鈻�

04/ Key indicators

Construction industry

The All Work material price index fell by 1.5% in the year to March 2015. Housing sector materials recorded inflation in March at just 0.1% over the year. Mechanical and electrical services materials also showed little price movement in the last 12 months. Falling metals commodity prices have made a primary contribution to this benign price environment for M&E related materials. Again, housing sector materials displayed stronger signs of any price inflation over the year, rather than disinflationary trends observed in the non-housing and repair and maintenance sectors.

| Construction materials | % change | |

|---|---|---|

| Mar 2014 - Mar 2015* | ||

| New housing | +0.1 | 鈻� |

| Non-housing new work | -2.2 | 鈻� |

| Repair and maintenance | -1.3 | 鈻� |

Mechanical services materials | ||

| Housing only | 0.0 | 鈻� |

| Non-housing | +0.5 | 鈻� |

| Electrical services materials | -0.5 | 鈻� |

| *provisional | ||

| % change | |

|---|---|

| Mar 2014 - Mar 2015* | |

| Imported plywood | +8.4 |

| Clay bricks | +8.2 |

| Ready-mixed concrete | +4.8 |

| Pre-cast concrete products | +4.6 |

| Crushed rock including levy | +4.5 |

| Pre-cast concrete products: bricks, blocks, tiles and flagstones | +4.4 |

| Other builders ironmongery | -0.7 |

| Insulating materials (thermal and acoustic) | -0.8 |

| Coated roadstone excluding levy | -2.2 |

| Imported sawn or planed wood | -5.7 |

| Concrete reinforcing bars | -9.9 |

| Fabricated structural steel | -10.6 |

| *provisional |

Data sources: ONS and BIS

UK economy

| Consumer prices | % change | |

|---|---|---|

| Apr 2014 - Apr 2015 | ||

| Consumer Prices Index (CPI) | -0.1 | 鈻� |

The annual rate of consumer price inflation fell to -0.1% in April 2015. This is the first time in recorded history, and since 1960 using comparable historic data, that this measure of inflation has turned negative.

| Industry input costs | % change | |

|---|---|---|

| Apr 2014 - Apr 2015 | ||

| Material and fuels purchased by manufacturing industry | -11.7 | 鈻� |

| Materials and fuels purchased by manufacturing industry excluding food, beverages, tobacco and petroleum industries | -3.1 | 鈻� |

While input prices fell annually to -11.7% in April, the pace of price deceleration dropped from a low of -14.1% in January 2015. Core input inflation, which excludes volatile items, posted -3.1% over the year, which was similar throughout Q1 2015. Crude oil and imported metals disinflation contributed towards the annual change in input prices. Sterling鈥檚 strength also accounts for lower imported commodity prices in the last year.

| Industry output costs | % change | |

|---|---|---|

| Apr 2014 - Apr 2015 | ||

| Output prices of manufactured products | -1.7 | 鈻� |

| Output prices of manufactured products excluding food, beverages tobacco and petroleum | +0.1 | 鈻� |

Factory gate prices continued to fall in April 2015 on a yearly basis, now 10 months successively. Output prices during Q1 2015 did level out, actually rising 0.1% between March and April, though the yearly metric remained firmly negative. The core index, which is narrower because it excludes items such as petroleum and food, increased just 0.1% in the year to April.

Source: ONS

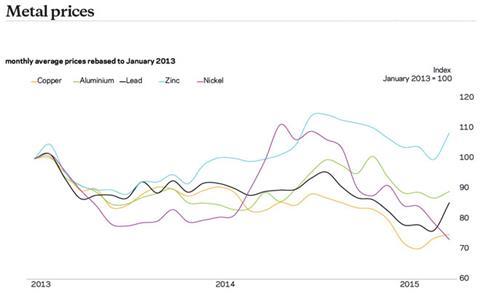

| % change Apr 2014 - Apr 2015 | ||

|---|---|---|

| Copper | -9.6 | 鈻� |

| Aluminium | +0.4 | 鈻� |

| Lead | -4.1 | 鈻� |

| Zinc | +8.6 | 鈻� |

| Nickel | -26.4 | 鈻� |

Although price falls across metal commodities continued into Q1 2015, copper, lead and aluminium saw some reversals in these trends. Zinc also followed suit with a price rebound, as closure of two large zinc mines introduced concerns that supply might be lower in the near-term. But other pricing factors for zinc appear to counteract this supply constraint narrative.

| April 2014 | April 2015 | ||

|---|---|---|---|

| average | average | % change | |

| Euro to sterling | 1.212 | 1.382 | +14.1 |

| US dollar to sterling | 1.673 | 1.492 | -10.8 |

Sterling鈥檚 long appreciation against the Euro ended in Q1 2015. Despite retaining most of its strength against the Euro, sterling sought a level around the 1.35 to 1.40 range in recent months. Similarly, the US dollar鈥檚 climb against sterling was halted towards the end of Q1 2015. Sterling has since recovered some ground against the US$, posting a recent high of US$1.57 in mid-May.

Labour

05/ Labour market statistics

- In March 2015, average weekly earnings (total pay including bonuses) in construction increased to 拢565 from 拢557 in March 2015. Annually, earnings rose 6.3% in March on a single-month basis, and 1.8% annually on a three-month average basis. Regular pay (excluding bonuses and arrears) increased at marginally slower annual rates of 5.5% and 1.7% respectively.

- Construction industry regular pay exceeded similar changes to average earnings for the whole economy. Total average weekly earnings for the whole economy measure were 拢489 in March, which represented an annual rate of change of 1.9% (three-month average basis).

06/ Wage agreements

Construction Industry Joint Council

The parties to the Construction Industry Joint Council have agreed a new pay deal, which saw pay rates increase by 3% from 30 June 2014, and a further 3% rise from 29 June 2015. Travel and fare allowances also increased from 30 June 2014, along with subsistence allowances increasing to 拢35 a night from 6 January 2015. The agreement also addressed changes to sick pay.

Joint Council Committee of the Heating, Ventilating and Domestic Engineering Industry

A 2.5% increase in hourly wage rates came into effect from 6 October 2014. Amendments to the basic working week also apply from the same date, as the number of hours per week reduces from 38 to 37.5. Changes to the level of weekly sickness and accident benefit are also planned.

The Joint Industry Board for the Electrical Contracting Industry

Members received a 2% pay rise in January 2015, which will be followed by a 3% increase from January 2016.

好色先生TV and Allied Trades Joint Industry Council

The 好色先生TV and Allied Trades Joint Industrial Council (BATJIC) agreed a two-year pay deal effective from 30 June 2014. The deal involves variable wage rises for the standard wage rates averaging 2.5%. A further set of rises averaging 3% come into effect from 29 June 2015. Annual holiday entitlement will increase by one day, as of 29 June 2015, from 21 days to 22 days, making a total of 30 days including public holidays.

The new BATJIC rates of wages are:

| Standard rates of pay for 39 hours per week | Per week | Per hour |

|---|---|---|

| S/NVQ3: Advanced | 拢436.80 | 拢11.20 |

| S/NVQ2: Intermediate | 拢376.35 | 拢9.65 |

| Adult general operative | 拢327.60 | 拢8.40 |

| For entrants aged 19 years and over | ||

| 拢344.37 | 拢8.83 |

| 拢299.52 | 拢7.68 |

| Apprentices under 19 years of age | ||

| 拢308.51 | 拢7.91 |

| 拢291.63 | 拢7.48 |

| WAGE AGREEMENT SUMMARY The following table summarises the wage agreements currently in force for the principal wage fixing bodies within the construction industry | |||||

|---|---|---|---|---|---|

| Operatives | Agreement body | Current basic hourly rate | Effective since | Details in | Date of next review |

| Builders and civil engineering operatives | Construction Industry Joint Council | Craft rate: 拢11.00 / hour | 30 June 2014 | Spon鈥檚 Architects鈥� and Builders鈥� Price Book 2015 | 29 June 2015 |

| 好色先生TV and Allied Trades Joint Industrial Council (BATJIC) | S/NVQ3 advanced craft: 拢11.20 / hour | 30 June 2014 | Spon鈥檚 Architects鈥� and Builders鈥� Price Book 2015 | 28 June 2015 | |

| Plumbers | The Joint Industry Board for Plumbing Mechanical Engineering Services in England and Wales | Advanced plumber: 拢14.06 / hour | 5 January 2015 | Spon鈥檚 Architects鈥� and Builders鈥� Price Book 2016 | 4 January 2016 |

| Scottish and Northern Ireland Joint Industry Board for the Plumbing Industry | Advanced plumber: 拢13.41 / hour | 6 July 2015 | Spon鈥檚 Architects鈥� and Builders鈥� Price Book 2016 | A two-year agreement: Year 1 2015 = 2.5% Year 2 2016 = 2.0% | |

| H&V operatives | Joint Conciliation Committee of the Heating, Ventilating and Domestic Engineering Industry | Craftsman: 拢11.84 / hour | 6 October 2014 | Spon鈥檚 Architects鈥� and Builders鈥� Price Book 2015 | 5 October 2015 |

| Electricians (national) | The Joint Industry Board for the Electrical Contracting Industry | Approved electrician: 拢15.16 / hour (own transport) | 5 January 2015 | JIB for the Electrical Contracting Industry | A two-year agreement Year 1 2015 = 2% Year 2 2016 = 3% |

| Scottish Joint Industry Board for the Electrical Contracting Industry | Approved electrician: 拢15.16 / hour (own transport) | 5 January 2015 | SJIB for the Electrical Contracting Industry | A two-year agreement Year 1 2015 = 2% Year 2 2016 = 3% | |

No comments yet